Absa Bank Kenya has responded to a customer who publicly complained of an unexplained debit from his bank account, reigniting discussion about how quickly banks should resolve disputed transactions and customer complaints.

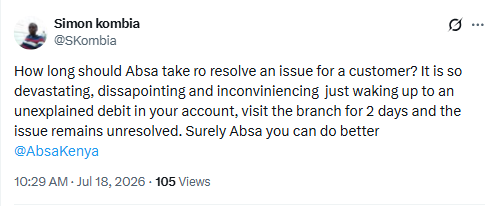

The customer, identified on X as Simon Kombia (@SKombia), questioned the bank’s handling of the matter after claiming he discovered an unexpected deduction from his account and spent two days seeking assistance at a branch without receiving a resolution.

“How long should Absa take to resolve an issue for a customer? It is so devastating, disappointing and inconveniencing just waking up to an unexplained debit in your account, visit the branch for two days and the issue remains unresolved. Surely Absa you can do better,” Kombia posted while tagging the bank’s official customer care account.

Absa apologises

Responding publicly to the complaint, Absa Bank Kenya acknowledged the customer’s frustration and apologised for the delay.

“Hello Simon, we highly regret the delay and inconvenience. We would love to make this right. Kindly check your DM and revert,” the bank replied.

The lender did not publicly explain the cause of the reported debit or indicate how long the investigation would take, instead requesting to continue the conversation through direct messages.

It also remains unclear whether the disputed transaction has since been reversed or resolved.

What customers should do

Financial experts advise customers who notice an unfamiliar debit on their accounts to report it immediately through their bank’s official customer service channels.

Customers are also encouraged to:

- Review their recent account activity to identify the transaction.

- Report the disputed transaction immediately.

- Keep transaction alerts, receipts and account statements.

- Obtain a reference number when lodging a complaint.

- Follow up regularly until the matter is resolved.

Where fraud is suspected, banks may temporarily investigate the transaction while verifying whether it was authorised or originated from a merchant, card payment or electronic funds transfer.

Consumer protection

Banks operating in Kenya are expected to maintain effective customer complaint handling mechanisms under regulatory requirements issued by the Central Bank of Kenya (CBK).

Customers who are dissatisfied with the handling of a complaint may escalate the matter through the bank’s internal dispute resolution process before seeking further intervention through the relevant regulatory or dispute resolution channels where applicable.

Consumer rights advocates have consistently called on financial institutions to improve response times for disputed transactions, noting that unexplained debits can cause significant financial hardship, especially where customers rely on their accounts for daily expenses or business operations.

Growing reliance on digital banking

The complaint comes at a time when millions of Kenyans increasingly rely on mobile and digital banking services for everyday transactions.

As digital payments continue to grow, banks have invested heavily in fraud detection systems and customer support to address disputed transactions, unauthorised debits and suspected fraudulent activity.

While most disputes are resolved after investigations, banking experts advise customers never to ignore unfamiliar deductions and to report them as soon as they are detected.

Absa Bank Kenya has not publicly disclosed the outcome of Simon Kombia’s complaint, but the bank has indicated that it is engaging him directly to resolve the issue.